3D Secure Retrospective: Exploring the Evolution and Future of Secure Online Transactions

The Early Days: Simpler Times, But Not Secure

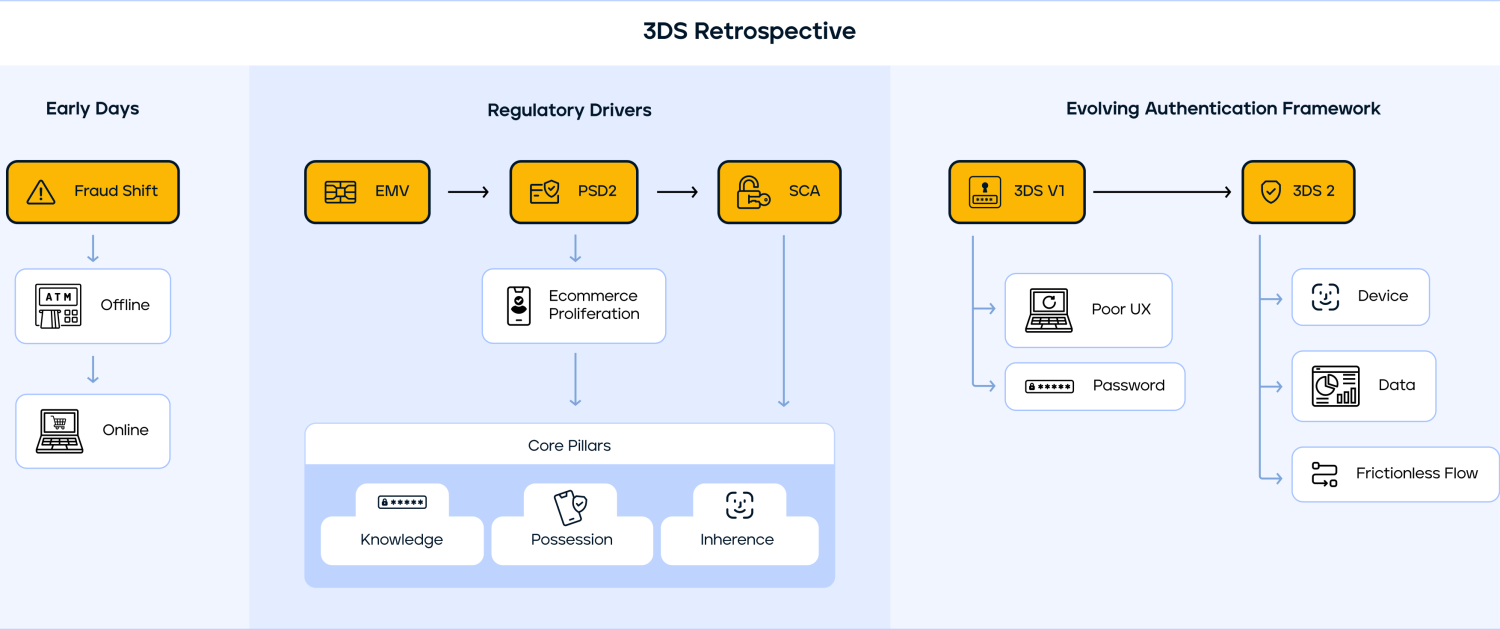

In the early days of digital transactions, security was not a primary focus due to the nascent technology and infrastructure. Traditional payment methods like debit and credit cards were optimised for in-person transactions and lacked the safeguards required for the unique risks of online payments.

The introduction of EMV (Europay, Mastercard, and Visa) standards marked a pivotal shift. EMV’s chip technology significantly improved transaction security, reducing fraud associated with card-present transactions. However, the rise of online payments brought unparalleled convenience and a new wave of threats, with fraudsters shifting their focus online. This period saw a surge in online fraud, necessitating more robust security measures in the digital payment landscape.

In response to these growing threats, the concept of 3D Secure (3DS) was introduced. 3DS aimed to provide an additional layer of security for online transactions by requiring cardholders to authenticate themselves during the payment process. This multi-factor authentication method helped mitigate the risks associated with online fraud, ensuring that transactions were authorised by the legitimate cardholder.

Historical Context

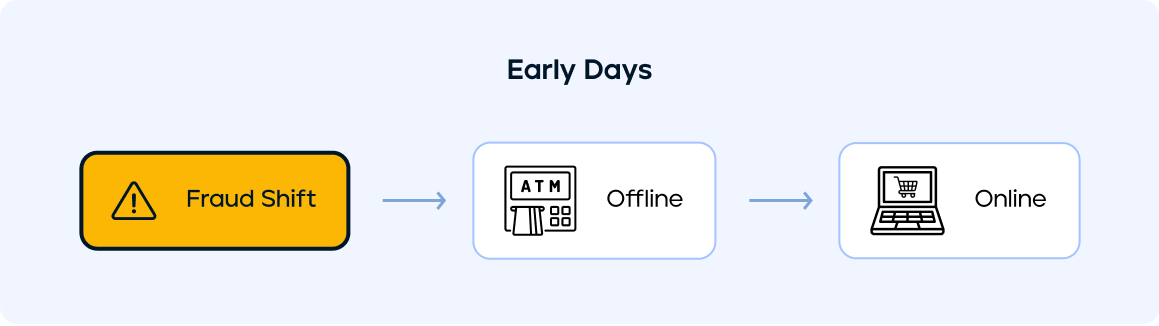

The initial need for 3D Secure (3DS) was driven by the rise in online transaction fraud and the pressing need for improved security measures. EMV standards had already enhanced security for card-present transactions by introducing chip technology, which significantly reduced the risk of fraud in physical transactions. However, as the online marketplace grew, it became clear that similar security measures were needed for digital transactions to protect against the increasing threat of online fraud. Existing security measures were inadequate for the unique challenges of remote transactions, where neither the cardholder nor their card is physically present.

To address this gap, the initial concept of 3-D Secure (3DS) was developed. 3DS added an extra layer of security by requiring cardholders to authenticate themselves during an online transaction, typically through a password or a code sent to their mobile device. This additional step helped verify that the person making the transaction was the legitimate cardholder, thereby reducing the risk of fraud and unauthorised transactions. This concept of multi-factor authentication became a crucial component in enhancing the security of online payments, providing the same level of trust and security that EMV had brought to physical transactions.

Influence and Regulatory Drivers of 3DS Development

The development and evolution of 3DS were heavily influenced by regulatory frameworks, particularly in Europe. The implementation of the Payment Services Directive 2 (PSD2) introduced Strong Customer Authentication (SCA), mandating stricter security measures for online transactions. These regulations significantly impacted the adoption and evolution of 3DS, driving its widespread implementation.

Interestingly, the adoption of 3DS varied across different regions. While Europe saw a high adoption rate due to regulatory mandates like PSD2 and SCA, other regions, such as the Middle East, experienced more gradual adoption, primarily due to diverse regulatory environments and the need for market education on the benefits of 3DS. Conversely, regions such as India and Ukraine are seeing a strong regulatory push for digital payment security, driven by government initiatives and financial reforms.

Technological Advancements and Innovations

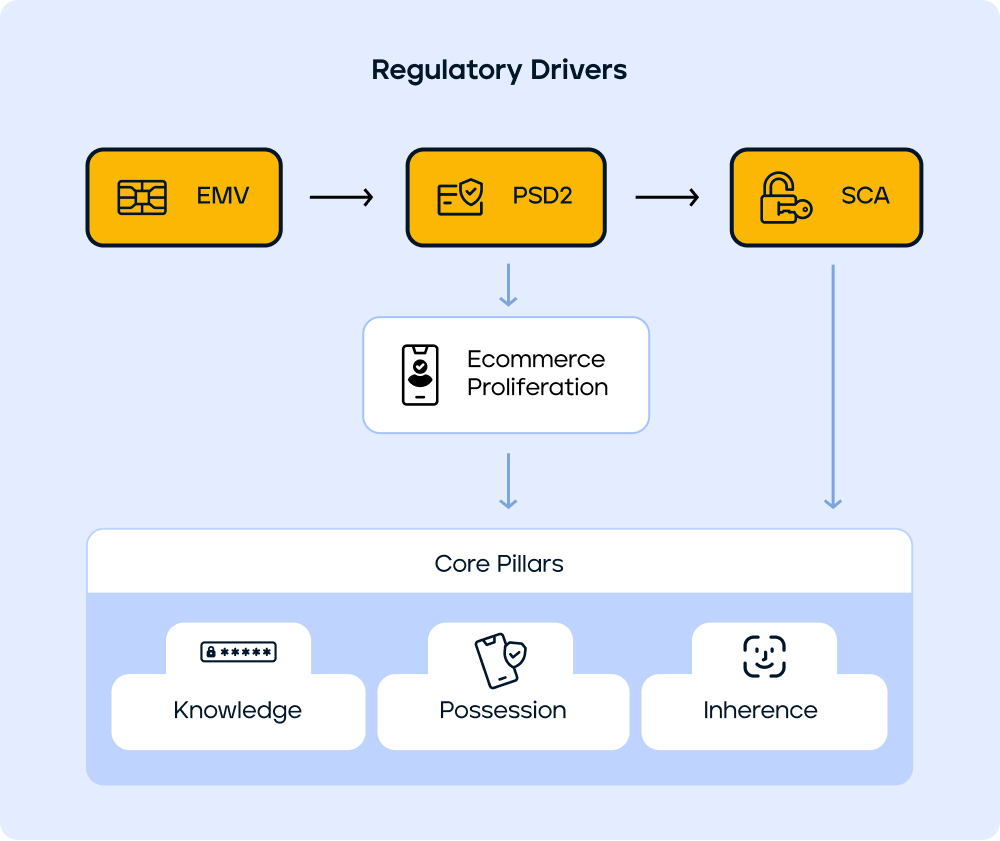

The journey of secure authentication began with the 3DS 1.0 framework, which has since evolved through versions 2.1, 2.2, and the current 2.3. The original 3DS framework, while effective, often resulted in a cumbersome user experience, with nearly all transactions being challenged. The shift from 3DS 1 to 3DS 2 was driven by the need to improve user experience and reduce transaction abandonment rates. By incorporating biometric authentication, risk-based decision-making, and broader device compatibility, 3DS 2 delivers a superior user experience while maintaining stringent security standards.

One of the key innovations in 3DS 2.2 is the introduction of tokenization, which enhances security by replacing sensitive card details with unique tokens. This process ensures that even if payment data is intercepted, it cannot be used fraudulently. Additionally, the initial validation process in 3DS 2.2 verifies card authenticity, significantly reducing the risk of fraud.

A major benefit of 3DS 2.0 is the liability shift. When a transaction is successfully authenticated using the 3DS framework, the fraud liability transfers from the merchant to the issuer. This incentivises merchants to adopt 3DS 2.0, as it reduces their risk exposure. However, adoption varies across regions due to differences in regulatory frameworks. While some regions enforce strict mandates for implementing 3DS 2.2, others have opted for more flexible approaches, resulting in uneven adoption rates.

3DS 2.0 introduced support for browser-based in-app payments, allowing users to complete transactions within the app without being redirected to an external site. This feature enhances user experience by keeping the payment process within the app’s interface, ensuring continuity and security.

Additionally, 3RI (3DS Requestor Initiated) expanded the 3DS capabilities to include merchant-initiated transactions. By essentially allowing merchants to initiate a transaction without the direct involvement of the cardholder, this is a departure from the traditional 3DS process where the cardholder is actively involved in the authentication process. 3RI has been a pivotal development that opens up a wider range of possibilities for merchants, especially in areas like subscription billing, recurring payments, and installment plans.

The 3DS technology has adapted to meet the unique challenges of different industries and use cases:

- In the Internet of Things (IoT) sector, is a prime example where the 3DS framework has been adapted to fit the IoT environment. Indeed, unlike traditional e-commerce, IoT devices often have limited processing power, battery life, and display capabilities. Additionally, the sheer number of connected devices creates a complex security landscape. enhanced authentication protocols ensure that each device in the network can securely verify its identity, preventing unauthorized access and potential breaches. 3DS leverages device-specific characteristics, like hardware identifiers and software versions, for risk assessment.

- By integrating 3DS, gaming platforms can implement an extra layer of security for online transactions. This involves authenticating the cardholder through various methods, such as password, biometric data, or one-time passcodes. This makes it significantly harder for fraudsters to complete unauthorized purchases, protecting both the gamer and the game publisher, without interrupting gameplay.

Biometric authentication and in-car payments represent the latest advancements in the field. Integrating fingerprint scanning and biometric data for secure authentication addresses the challenges of multiple users in shared environments like cars. This innovation ensures that only authorised users can complete transactions, enhancing overall security.

User Experience and Necessary Friction

Striking the right balance between security and user convenience remains a core challenge in the authentication process. Maintaining high security standards without making the process overly complicated for users is essential. Low-friction methods, like entering a one-time password (OTP) sent to a mobile phone, enhance security while adding minimal inconvenience to the transaction process.

With the rise of Account-to-Account (A2A) transfers, the focus often revolves around their efficiency and convenience. However, it is important to consider what is being sacrificed in this process. When a user directly transfers money to a merchant’s account, resolving issues such as refunds, fraud, or receiving incorrect products can become problematic without an intermediary. Intermediaries such as PayPal are crucial in these scenarios as they provide a buffer between the customer and the merchant. This layer of protection is essential in the transaction ecosystem and introduces necessary friction to ensure consumer protection. This is precisely where 3DS sits. Minimal friction methods, such as entering a one-time password (OTP), offer significant benefits by maintaining security without overly complicating the user experience.

Even with the latest technological advancements, such as tokenisation, 3DS remains essential. Tokenisation replaces sensitive card details with unique tokens to enhance security. However, 3DS is still needed in the initial phase to validate the card’s authenticity. Some industry experts advocate for newer methods of security, but these approaches often lack the maturity and reliability of established systems such as 3DS. Although these new methods show promise, they are not yet robust enough to function independently. Therefore, the industry must balance adopting innovative technologies with maintaining proven security measures like 3DS to protect all stakeholders effectively.

Future Directions

As online fraud continues to evolve, the need for robust authentication measures remains critical.

In retrospect, the journey of 3DS authentication from its inception to the present day underscores the continuous evolution of security measures in response to emerging threats. Regulatory influences, technological advancements, and user experience considerations have all shaped the current landscape of 3DS. As the digital payment ecosystem continues to evolve, the role of 3DS in ensuring secure and seamless transactions will remain indispensable, highlighting the ongoing need for innovation and industry collaboration in combating online fraud. Collaboration and innovation within the industry will be key to addressing emerging threats and maintaining trust in digital transactions.